Headlines:

- Gas and Electricity Wholesale prices are slightly lower than last week

- EU Gas Storage levels are 61% full compared to 76% last year

- Lower Storage levels are creating nervousness for this winter and 2025/26

Energy Overview

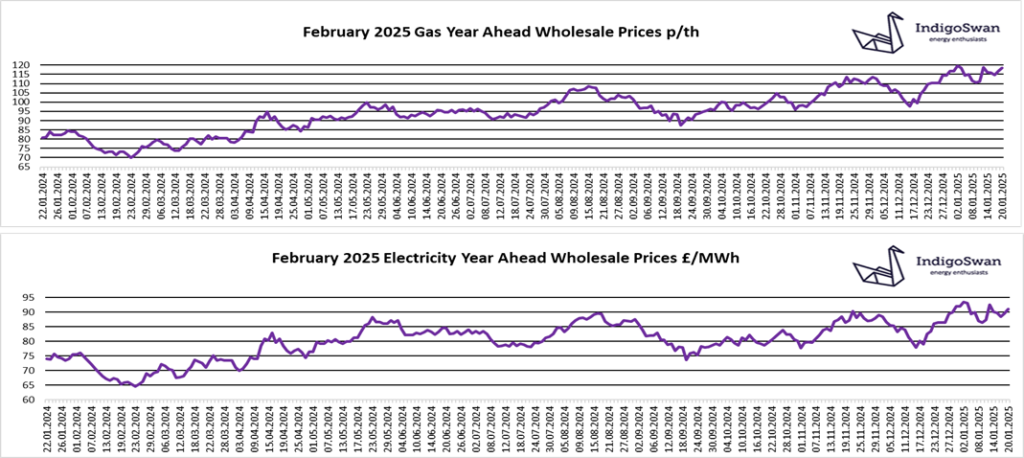

Gas and Electricity Year Ahead Wholesale costs are slightly lower than last week. They are similar to 2024, showing good value compared to most of 2021 / 2022 / 2023, but are more than double 2020. The Oil price is lower at $80.

Energy markets are still incorporating the concern for Gas Storage levels, both in the UK and the EU, where they are just 61% full compared to 76% last year. From January, the EU no longer receives Gas from Russia via Ukraine due to the end of the transit deal. This has meant a greater use of Storage to help meet demand during colder spells. Although we are seeing increased LNG deliveries, global competition is high, and a premium has to be paid to secure shipments. This will make it expensive to replace Storage during the warmer months, in readiness for winter 2025/26. Some EU members are keen to see a reduction of, or the complete ban of Russian LNG deliveries, which continue to increase. Any Gas purchased from them provides revenue to support their invasion of Ukraine. Realistically, the EU still needs Russian Gas, so for the time being, restrictions would likely be opposed. President Trump has confirmed his policy to further develop their LNG infrastructure and is encouraging the EU to buy from them rather than cheaper Gas from Russia, or face tariffs. This could mean that the EU needs to be creative and make Gas from Russia less attractive than from the US.

To add additional pressure to both Gas demand and Electricity prices, over the last week its use for generation has been a very high 55% of supplies, due to Wind being just 16%, falling as low as just 6% on the 20th.

Milder temperatures are due across Europe which may help to reduce supply concerns, but when we have seen the beginning of a downward trend, this has quickly turned to volatility due to tight supply margins. We would encourage customers that have Gas or Electricity contracts ending in the first half of 2025, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog, why not try one of our others: