Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- EU Gas Storage levels are a positive 62% full

- There is the potential for price volatility

Energy Overview

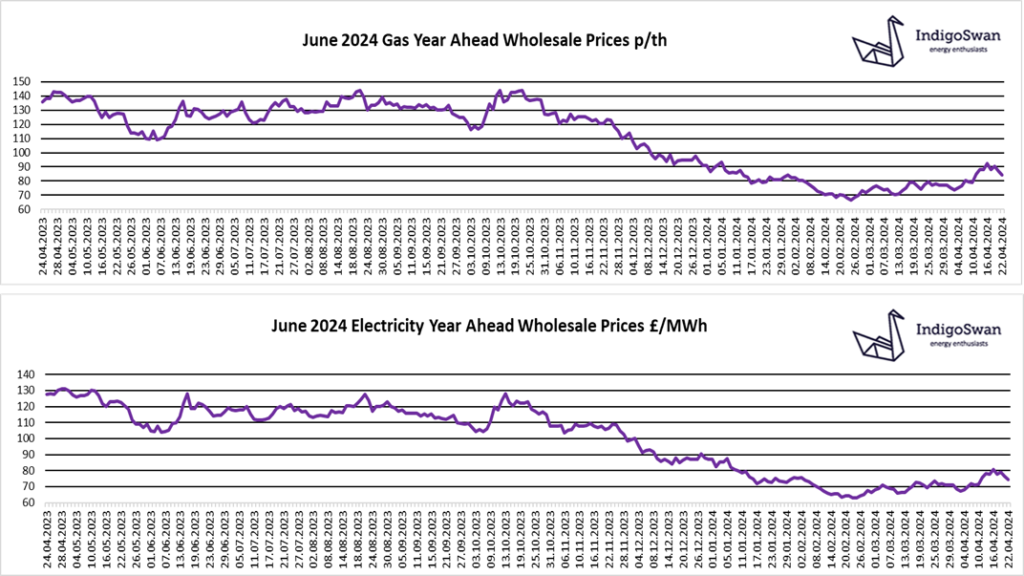

Gas and Electricity Year Ahead Wholesale costs are lower than in last week’s report. There is a small premium for longer term contracts.

Some of the concern that has been built into energy prices has eased, with what appears to be reduced tensions between Iran and Israel, as the most recent military action has been downplayed by both parties. The increase in Russia’s airstrikes against Ukraine’s energy infrastructure and an expected push this summer, have also been a factor, but with the US pledging a huge aid package to Ukraine, this may stall progress.

The use of Gas for Electricity generation increased over the last week to 19% as did Imports from Europe at 17%, whilst Wind fell from 42% to 25%. The EU Gas Storage target of being 90% full by November, looks likely to be exceeded again, as it is currently 62% compared to 57% last year. LNG deliveries continue to arrive to help offset the reduction in Gas flows from Russia, since tensions began in 2021. The US Freeport Gas LNG plant is set to resume exports after issues earlier in the month.

It is expected that temperatures will be below seasonal norm over the next week, which will add some pressure to Gas supplies through additional heating demand. It is also likely that Wind’s contribution to generation will be lower.

With energy markets reacting to any hint of supply or demand issues, we would encourage customers that have Gas or Electricity contracts that end in 2024, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog, why not try one of our others: