Headlines:

- Gas and Electricity Wholesale prices are slightly higher than last week

- EU Gas Storage levels are a very positive 95% full

- Uncertainty as to price direction as we head towards the winter

Energy Overview

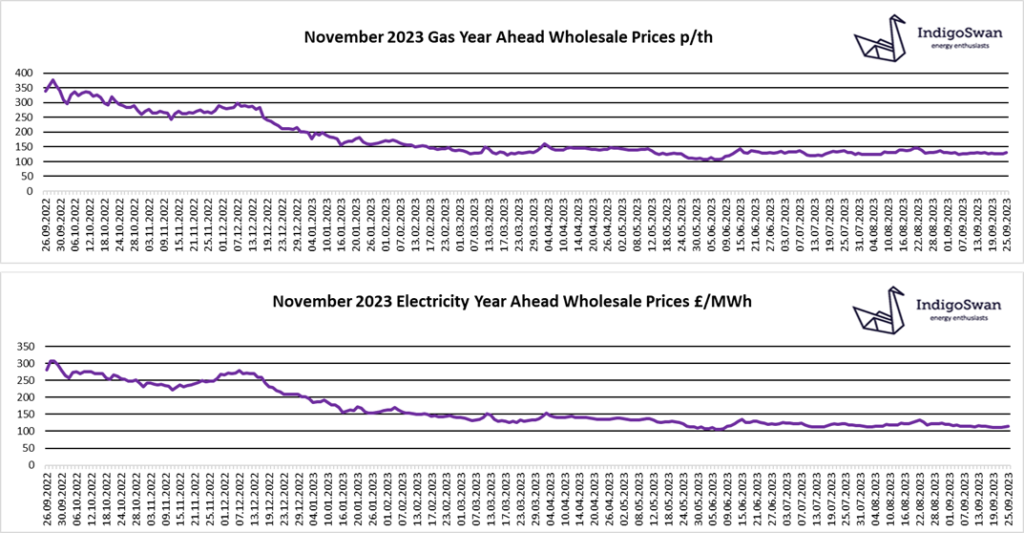

Gas and Electricity Wholesale costs are higher than last week.

Despite the ending of the industrial action in Australia last week, which had threatened to disrupt up to 7% of global LNG supplies, Gas prices did not fall as may have been expected. This is most likely due to the strike action having no significant impact on deliveries and extended Norwegian Gas supply outages. EU Gas Storage levels are now 95% full compared to 94% last week and a target of 90% by November. Much of last year’s inflated pricing was due to Storage being just 87% full and a concern that a harsh winter would result in supply restrictions. This did result in a change in consumer habits and a lower energy use. If we have a prolonged period of very cold temperatures, we could once again see price increases as Europe competes with Asia for LNG deliveries.

Electricity prices continue to follow Gas, as Gas remains a major and reliable source of generation, although at a much reduced 22% of supplies over the last week, compared to the previous 36%. Wind accounted for a high 33%, peaking at over 50% on Sunday. Imports via the interconnectors supplied 12% and Coal remains an important asset to balance the network as we head towards the winter.

Prices remain stubbornly high with little indication that this will change in the short term. Energy markets are overreacting to any supply issues, which could potentially mean a period of volatility through the winter, although unlikely to be as extreme as 2022. For this reason, Indigo Swan are advising customers to review contracts that end in 2023 or early 2024.

If you enjoyed reading this blog, why not try one of our others: