Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- EU Gas Storage levels are a very positive 93% full

- Uncertainty as to price direction as we head towards the winter

Energy Overview

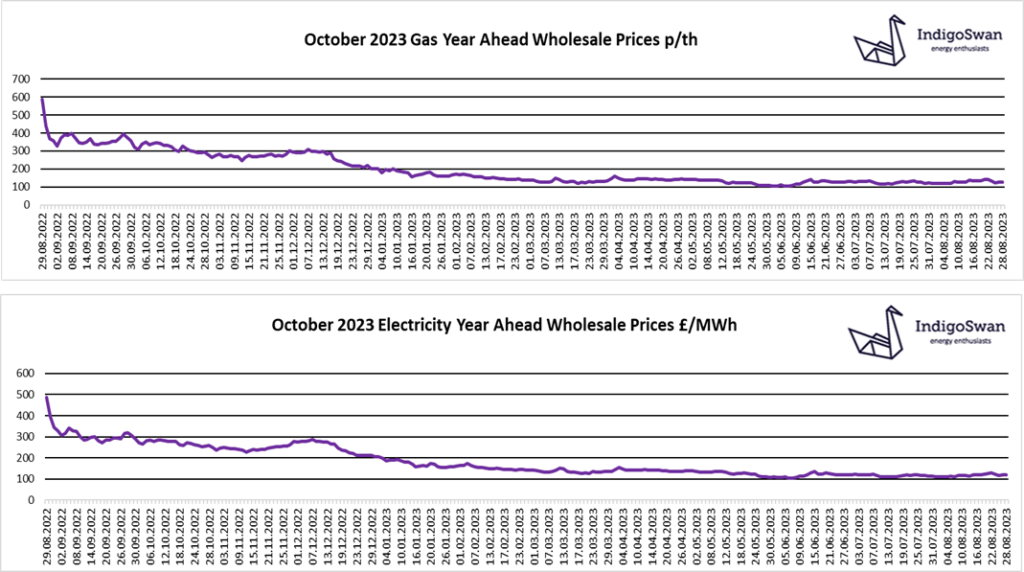

Gas and Electricity Wholesale costs are lower when compared to last week.

Following the news on the 9th of August that workers at Australian LNG plants may strike, there was an upward price reaction, with concerns that a reduction in deliveries to Asia may increase competition for those from the likes of Qatar and the US. Markets had begun to feel more optimistic for a positive outcome, and prices started to fall. However, on the 28th of August it was confirmed that strikes will take place on the 7th of September, and we are once again seeing some increases.

EU Gas Storage levels are 93% full, already exceeding the 90% target for November. This very healthy position has reduced some of the impact that the strikes may have had and provides confidence for the winter, when demand increases.

Electricity prices will continue to follow Gas, as it remains a major and reliable source of generation, at 45% of supplies over the last week. Wind’s low contribution at just 12% has meant the continued use of Coal and underlines the importance of Imports from the continent via the Interconnectors.

Compared to 2022 there has been little price movement in 2023, but we are still seeing daily swings and the potential for prices to move in either direction. Indigo Swan are advising customers to review contracts that end in 2023 or early 2024, to avoid exposure to potential market volatility.

If you enjoyed reading this blog, why not try one of our others: