Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- EU Gas Storage levels are a positive 62% full

- There is the potential for price volatility

Energy Overview

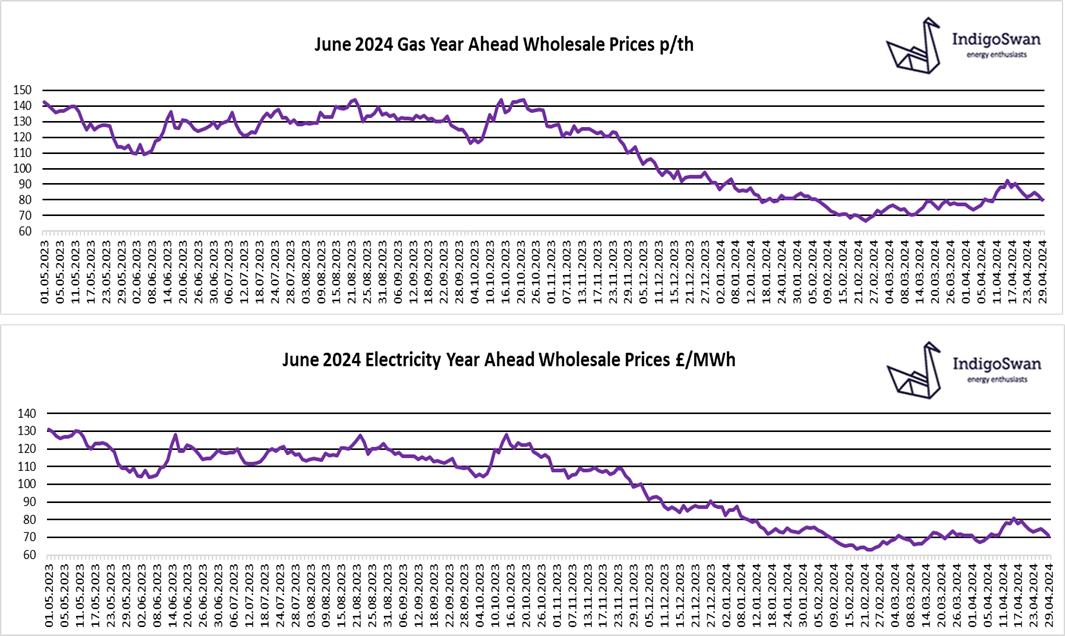

Gas and Electricity Year Ahead Wholesale costs are lower than in last week’s report. There is a small premium for longer term contracts.

Prices continue to struggle to find direction, although the last two weeks has seen a downward trend, after a small spike mid-month. Tensions in the Middle East have eased, avoiding further military action between Israel and Iran. A US aid package may help relieve pressure on Ukraine, following Russian attacks on their energy infrastructure. Both conflicts still have the potential to add volatility to energy prices if there is the possibility of disruptions to supplies.

Cooler temperatures last week meant an increased heating demand, stalling injections into Gas Storage. Levels remain high in the EU at 62% full, compared to 59% last year and a 90% target for November, which looks likely to be achieved. Fewer LNG deliveries are booked, but this is partially due to the positive supply position. The EU is considering widening their sanctions, from allowing individual members to ban Russian Gas, to restrictions for all members. There may be objections from those countries that remain reliant on Russian Imports.

A reduced Wind contribution over the last week at 19% of supplies, meant the need for more Gas generation at 27%. Imports from Europe through the Interconnectors remained high at 18%.

With energy markets reacting to any hint of supply or demand issues, we would encourage customers that have Gas or Electricity contracts ending in 2024, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog, why not try one of our others: