Headlines:

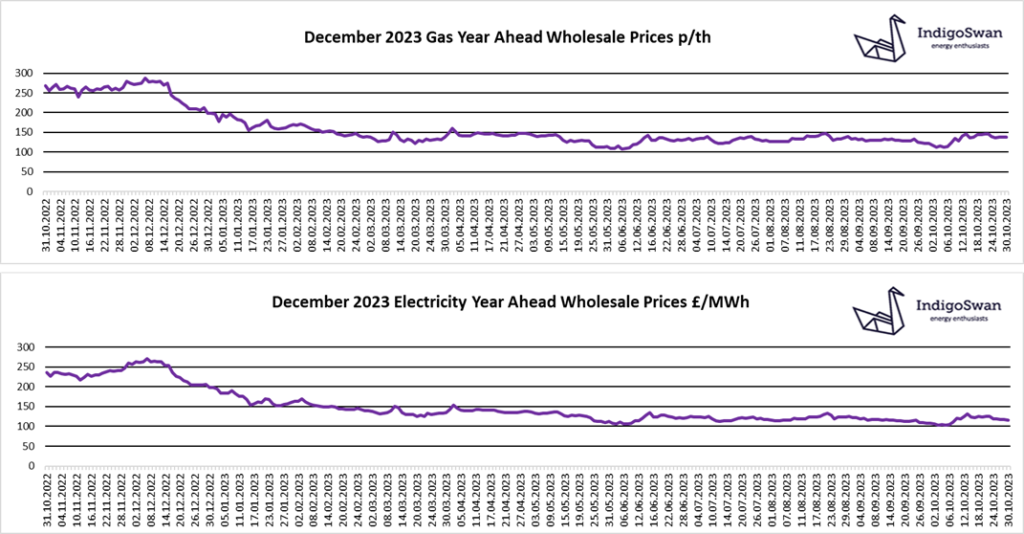

- Gas and Electricity Wholesale prices are lower than last week

- EU Gas Storage levels are a very positive 99% full

- Global events may create further price volatility

Energy Overview

Gas and Electricity Wholesale costs are lower than last week.

There is still an element of uncertainty about how the conflict in the Middle East may impact global energy supplies and prices, especially should it further destabilise the region. For now, markets have settled. An investigation into the damage of the Gas pipeline between Finland and Estonia has found that this was done by a ship’s anchor. It has yet to be determined if it was a deliberate act of sabotage, as we saw with Nord Stream in September 2022, or an accident. However, the possibility that this was unintentional has reduced the concern that other Interconnectors could be targeted.

EU Gas Storage levels are at 99% full, far exceeding the 90% target for November, when it becomes likely that a higher demand for heating and additional Electricity generation, may mean Gas withdrawals. The UK is in a similar position with high Storage levels, although our capacity is far lower than the likes of France, Germany and Italy, despite Rough being available. This underlines the importance of LNG deliveries to us and Europe, to compensate for the reduced flows of Russian Gas. Over the last week there has been a lower contribution from Wind at 23% compared to 33% the previous week, which has meant an increase in the use of Gas at 33% from 26%. The Electricity Interconnectors with the continent see us both Import and Export, but unlike last year when there were issues with French Nuclear reactors, we have been net importers.

Indigo Swan are advising customers to review contracts that end in 2023 or early 2024.

If you enjoyed reading this blog, why not try one of our others: