Headlines:

- Gas and Electricity Wholesale prices are higher than last week

- EU Gas Storage levels are a very positive 87% full

- Uncertainty as to price direction as we head towards the winter

Energy Overview

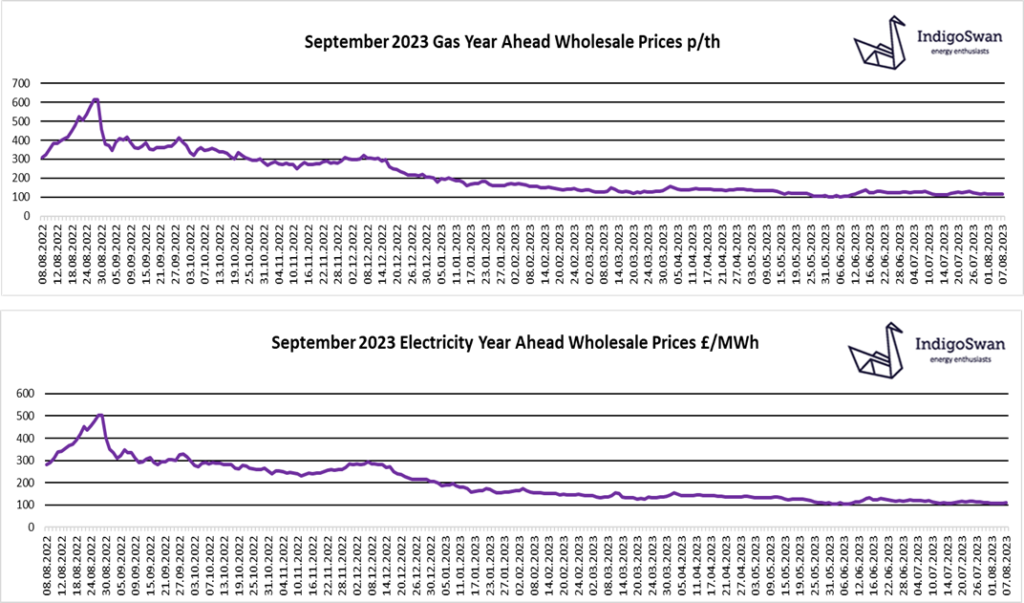

Since our last Energy Report, Gas and Electricity Year Ahead Wholesale prices are higher.

Following the large price drops in January, they are significantly lower than those we saw in 2022, although there has been little price movement in the last six months. Customer’s budgets are still being impacted by daily volatility which underlines the benefit in looking at the market for the best renewal options and either driving down the current supplier’s costs or switching.

EU Gas storage is currently 87% full against a target of 90% by November. This is a much more positive position than last year’s 72%, when there was a high degree of uncertainty if enough Gas could be sourced and how we would cope with the winter demand for heating and Electricity generation. Gas continues to flow from Russia and imports are being received via LNG shipments to new terminals, from the likes of the US, Africa and the Middle East. Should there be an increased demand from Europe or Asia due to prolonged periods of excessive hot or cold weather, this could place a price premium on LNG.

Last week saw a good supply of Wind generation at 23% which meant less reliance on expensive Gas at 30%. Electricity imports from the continent via the Interconnectors were a very high 20%.

Indigo Swan are advising customers to review contracts that end 2023 or early 2024 as there is a lack of clear price direction and the risk of increases as we head towards the winter with the potential for supply and demand issues.

If you enjoyed reading this blog, why not try one of our others: