Headlines:

- Gas and Electricity Wholesale prices are higher than last week

- EU Gas Storage levels are a positive 60% full

- Any new supply concerns may still create price volatility

Energy Overview

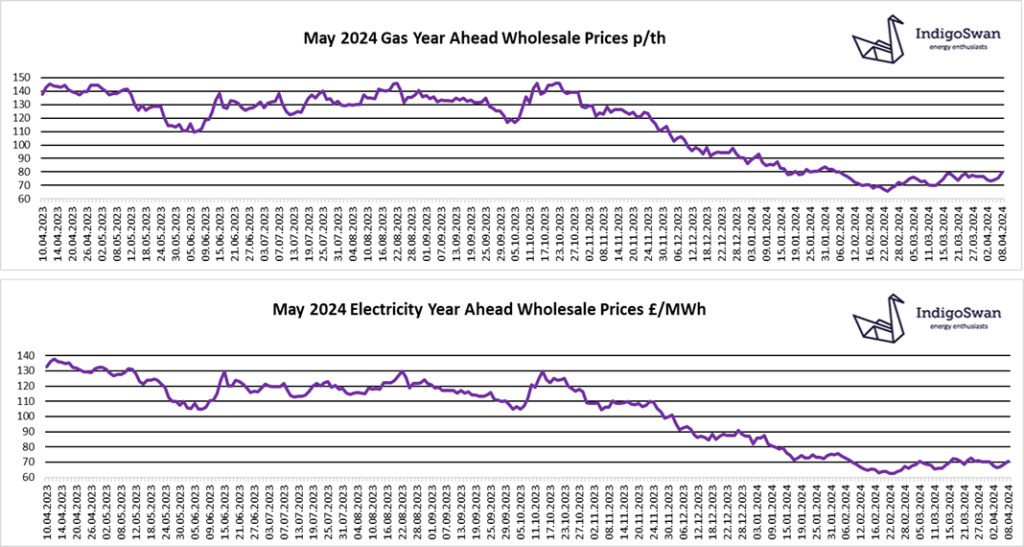

Gas and Electricity Year Ahead Wholesale costs are higher than in last week’s report. There is a small premium for longer term contracts due to various uncertainties.

Prices are struggling to find direction, showing daily swings, but remain considerably lower than 2023, 2022 and six months of 2021. It was hoped that the lower costs we saw in February would continue as we moved into Spring, but they have remained in the region of 10% higher, despite there being no significant issues. This underlines the potential for volatility should an event take place that impacts on energy supply or demand.

The mild temperatures have allowed Gas to be injected into EU Storage, currently at 60% full, which is 5% more than last year and a positive sign that once again the November target of 90% will be achieved. As the flows of Russian Gas into Europe are far lower than before tensions, it makes us heavily reliant on LNG shipments.

The use of Gas for generation has been lower over the last week at just 18% of supplies, with Wind’s contribution at 35%, peaking the weekend at 50%. Net Imports from Europe via the Interconnectors were high at 17%, although we were Exporters on Sunday due to strong winds.

From April 2024, Electricity Transmission and Balancing charges were lower and Distribution higher, which may overall have little impact. We are expecting further changes from April 2025.

We would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

If you enjoyed reading this blog, why not try one of our others: