Headlines:

- Below seasonal norm temperatures are forecast.

- The number of LNG shipments will be an important factor in price direction.

- Gas Storage levels are likely to come under renewed pressure.

Energy Overview

As of the 6th of April, Gas and Electricity Year Ahead Wholesale costs are higher, when compared to last month’s report.

Although Oil did reach almost $70 a barrel in March, it has since settled back down to $62. There have been some positive economic indicators, but these are outweighed by the increase in coronavirus cases, new lockdowns, and the decision by OPEC+ to further increase Oil production from May.

Gas prices remain volatile, reacting more recently to the new cold spell. Storage levels have improved but will now come under renewed pressure for heating demand. With unplanned Gas supply outages, the number of LNG deliveries and Storage levels will be monitored closely and determine the direction of the Wholesale price. There is also a need to start diverting Gas into Storage for the next prolonged cold spell.

As Gas contributed a high 40% to generation in March, there was a similar increase in Electricity prices, despite Renewables supplying around 50% on Bank Holiday Monday. Electricity will likely continue to follow Gas.

The Met Office forecast for the next month has a great deal of uncertainty but would indicate that April’s temperatures will initially remain below seasonal norm, then potentially reaching average.

What does this mean for me?

Wholesale prices for 2021 are very high when compared to 2020 but are comparable to 2018. Prices for 2022 and 2023 show much better value. It should be remembered that the Wholesale element makes up in the region of just 40% of the total cost of an Electricity bill and roughly 60% for Gas.

Increasing third-party costs are noticeable in Electricity contracts. These include, Transportation, Distribution, and government policy levies, which ensure we have enough energy to meet demand and provide investment.

Over the next year or two, the way some of these charges are calculated will change, under the Targeted Charging Review. Energy suppliers will be looking at their Electricity contracts and deciding whether to fix costs, pass them through or leave enough scope for them to decide, as they feel able. This does allow for the possibility of a review of some fixed price Electricity contracts from April 2022.

If temperatures remain low over the next month, we will likely see the continued need for high volumes of Gas to provide heating and potentially to support generation. This would indicate continued pressure on Gas and Electricity Wholesale prices.

We would advise looking at your options for contracts ending 2021 and potentially incorporate lower future prices.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

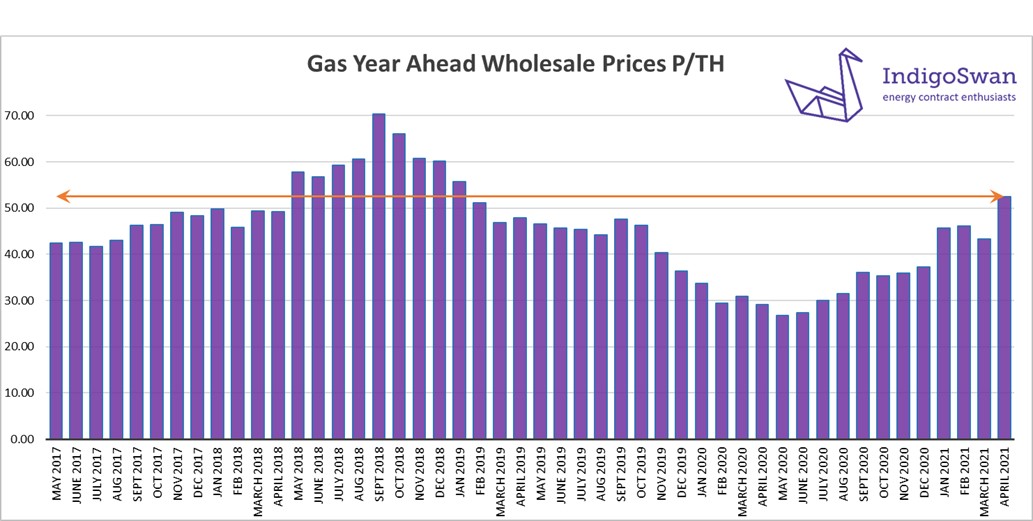

Gas Market Overview

On the 6th of April, the Gas Year Ahead Wholesale cost was 52.47 (p/th), from 43.25 (p/th) in last month’s report and 80% higher than 2020.

Gas supplies have been required to meet the heating demand from another cold spell and to support Electricity generation, which increased from 35% in February to 40% in March.

Storage did recover above 2020/21 levels in March during a mild period, but once again may be required over the coming weeks due to low temperatures and unplanned supply outages. Any surplus Gas will be injected into Storage for this coming winter, which helps create short term demand and price support, but gives more confidence longer term.

The number of LNG deliveries will be an important factor in price direction as will the extent that Gas will be required for generation. Although there was a significant fall in the price being paid for LNG in Asia and the return of shipments to Europe, being a global commodity, there is always a concern as to its reliability.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

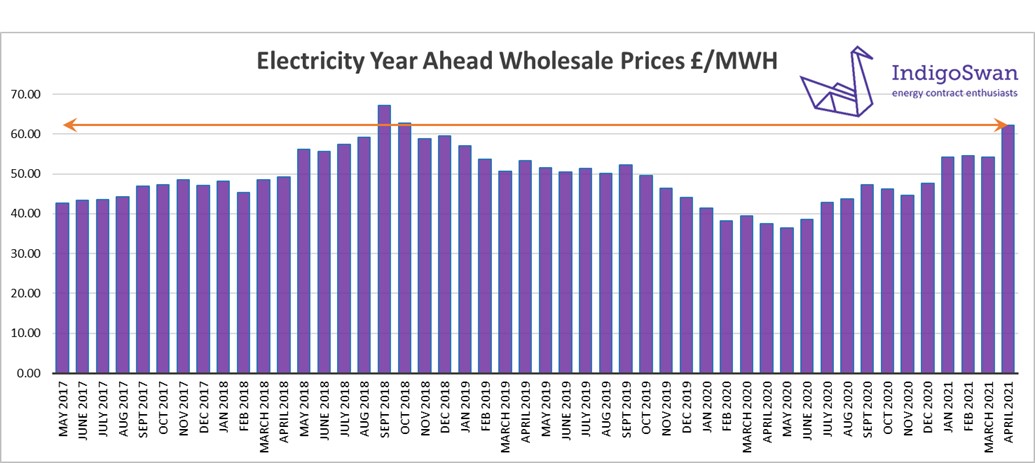

Electricity Market Overview

On the 6th of April, the Electricity Year Ahead Wholesale cost was 62.23 (£/MWh), from 54.13 (£/MWh) in last month’s report and 66% higher than 2020.

This increase has been driven by the higher Gas Wholesale cost, as it provided 40% of generation in March. As long as the cold period lasts and Gas Storage levels remain under pressure, there will be little optimism for significantly lower prices.

During March, Wind provided a reduced contribution of 20% from 26% in February, although there were days when it reached 40%. However, this erratic supply tends to have a minimal impact on longer term contract prices, rather the markets focus on the multiple national and global signals.

The industry remains confident that it can cope with demands, despite the nature of Renewables. Coal generation has not been required over the last two weeks and it was announced that another plant will close in 2022 before the complete end of Coal’s use by 2024. The National Grid has mechanisms in place, to secure additional supplies or reduce demand. These do come at a cost, in the form of higher third-party charges within Electricity bills but provide an element of stability to prices which otherwise may react far more dramatically.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.