Headlines:

- Very low gas storage levels

- Shortage of LNG deliveries

- Wind’s contribution to generation continues to be low

Energy Overview

As of the 5th of July, Gas and Electricity Year Ahead Wholesale costs are higher, when compared to last month’s report.

Oil has reached its highest point since late 2018 at $77 per barrel. OPEC+ have been reducing the extent of their production cuts, but July’s meeting ended with no agreement which could see the planned production increases in August, delayed. The talks to find agreement for the nuclear deal between the US and Iran have stalled. Should these succeed, we would expect additional Oil supplies to be available which may ease prices.

Gas prices have been extremely volatile due to the concern for the availability of Gas Storage this coming winter. As Gas is the main source of generation, Electricity prices have followed.

We should have started to inject Gas into Storage from April, however, due to colder temperatures, high Gas and Electricity demand, supply disruptions, a lower Wind contribution and the need to use Gas for Electricity generation, this has been delayed. Storage levels are 75% lower than last year.

The Met Office forecast for the next month suggests temperatures just above seasonal norm. However, there is little indication of the significant winds we need to reduce the burden on Gas for generation.

What does this mean for me?

Wholesale prices for 2021 and early 2022 are very high when compared to recent years. Prices for later in 2022 and 2023 show much better value. Generally, the Wholesale element makes up in the region of just 40% of the total cost of an Electricity bill and 60% for Gas, but these percentages will be higher for this volatile period.

Increasing third-party costs are noticeable in Electricity contracts. These include Transmission, Distribution, and government policy levies, which ensure we have enough energy to meet demand and provide investment.

Over the next year or two, the way some of these charges are calculated will change, under the Targeted Charging Review. Energy suppliers can choose whether to fix Electricity contract costs, pass them through or leave that decision until a later date. This does allow for the possibility of a review of the Distribution charges in some fixed price Electricity contracts from April 2022. It is very likely the Transmission element will be delayed until April 2023.

It looks unlikely that we will see a significant increase in Wind’s contribution to generation in the next month, meaning the continued reliance on Gas. The number of LNG deliveries are expected to be low and Gas supply maintenance is scheduled in July. With the need to put Gas into Storage, prices will likely continue to be high.

We would advise looking at your options for contracts ending 2021 and potentially incorporate lower future prices.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas market overview

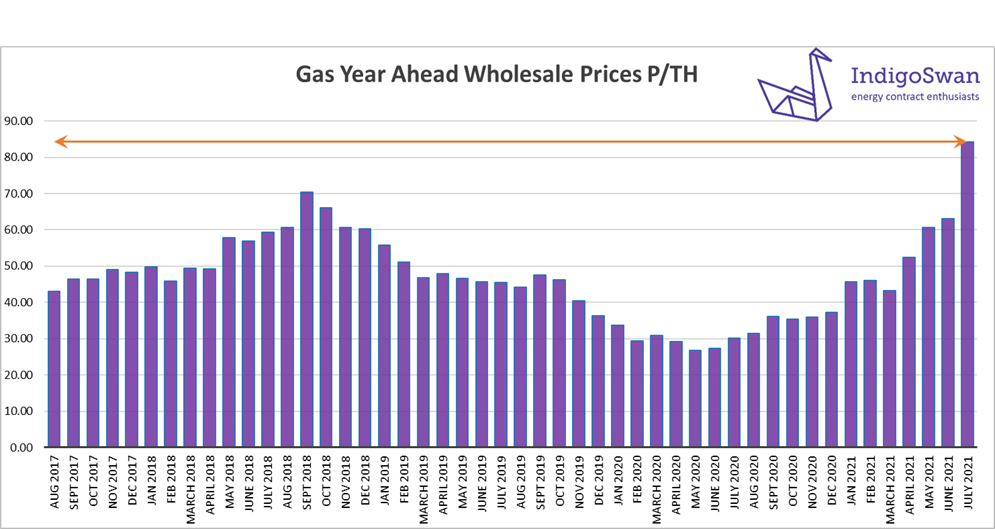

On the 5th of July, the Gas Year Ahead Wholesale cost was 84.28p/th, up from 63.08p/th in last month’s report and 180% higher than 2020. Prices from quarter two of 2022 are considerably lower.

The extremely low levels of Gas Storage at 25% of 2020, continue to dominate price direction. There have been a number of very cold spells creating surges in demand and even over the last week, when we should be injecting into Storage, we were withdrawing. This creates a great deal of nervousness as to if or when we will be able to increase levels sufficiently and at what cost, as we compete for Gas on an international market.

LNG has been a useful substitute for our reduced Storage capacity, but global demand is increasing and there are supply disruptions. If we want deliveries, we may need to outbid other countries which will likely see our Gas and Electricity Wholesale prices increase further.

The seasonal norm temperatures due this month should avoid any excessive demand on Gas for heating, although a potentially low Wind contribution would likely see a high demand for Electricity generation.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

Electricity market overview

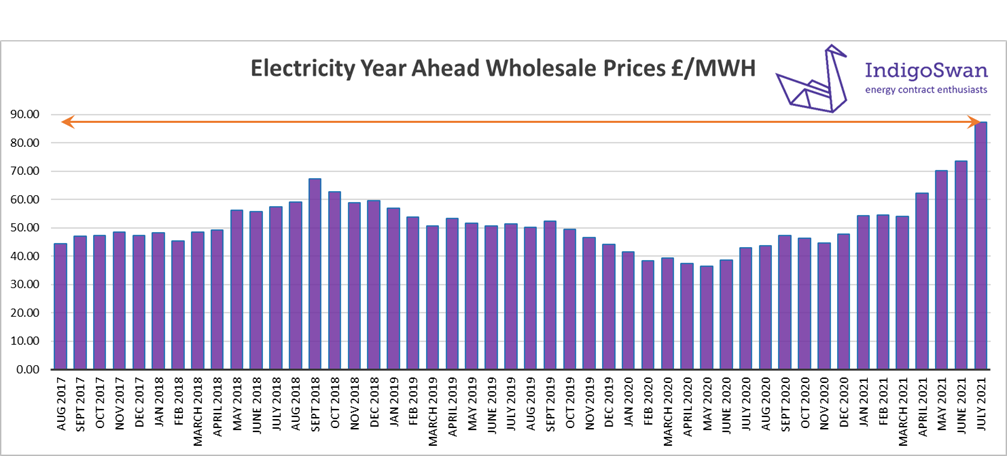

On the 5th of July, the Electricity Year Ahead Wholesale cost was £87.41/MWh, up from £73.45/MWh in last month’s report and 104% higher than 2020. Prices from quarter two of 2022 are considerably lower.

There are a number of factors which are contributing to this.

Gas continues to be the main source of Electricity generation, at 37% in June but 45% last week, which saw a considerable increase in Wholesale costs. This dependence on Gas means that with the very low Gas Storage levels and a concern for supplies this Winter, Electricity prices will potentially see further volatility.

Wind provided just 6% of generation last week and 12% in June, down from 15% in May. Its erratic nature does mean other sources need to be available, such as Gas and Coal. The use of carbon-based generation includes the need for carbon allowances, which have recently hit a record high, adding a further price pressure.

The National Grid has mechanisms in place, to secure additional supplies or reduce demand. These do come at a cost, in the form of higher third-party charges within Electricity bills but provide an element of stability to prices which otherwise may react far more dramatically.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts