Headlines:

- Wholesale prices for 2023 and 2024 show better value.

- EU Gas Storage levels are an improved 55% full.

- Prices are still being driven by concerns for Gas supplies into Europe.

Energy Overview

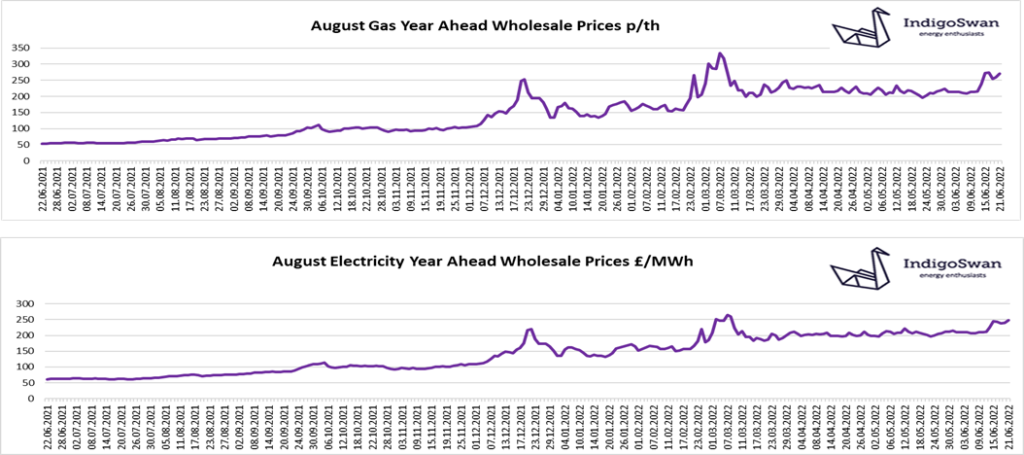

Since our last Energy Report, Gas and Electricity Wholesale prices are higher.

Costs for the remainder of 2022 are very high but show better value in 2023 and 2024, which does provide an opportunity to contract longer and reduce the shorter term % increases.

Prices continue to be pressured higher with the disruption of LNG supplies from the US for three months, due to the fire at the Freeport plant. Russia also announced the need for maintenance of the Nord Stream 1 Gas pipeline, which has been disputed by a number of parties, who see the reduced Gas flows as an attempt to create instability and push prices higher. These combined events cast some doubt on the opportunity for the EU to meet the Gas Storage target of 80% full by November, which is currently at 55%, up from 53% last week and 44% last year. Low Storage levels create a nervousness heading into the winter, due to the higher demand.

Several smaller consuming countries have had their Gas cut off as they refused to pay Russia in roubles. The potential that more countries may be added or that the EU members may find agreement and include Gas in their sanctions against Russia, is adding a considerable premium.

Electricity prices will follow Gas due to it being our main source of generation, at a high 44% so far in June.

We would advise looking at your options for contracts ending in Q3 and monitoring the remainder of 2022, having conversations with your contact at Indigo Swan about your specific requirements.