You are likely to have noticed that Gas and Electricity Wholesale costs are currently showing a premium for Winter 2021. So, what is causing this? Most people would agree, the driving factor is the very low level of Gas Storage and the concern for its availability this coming winter.

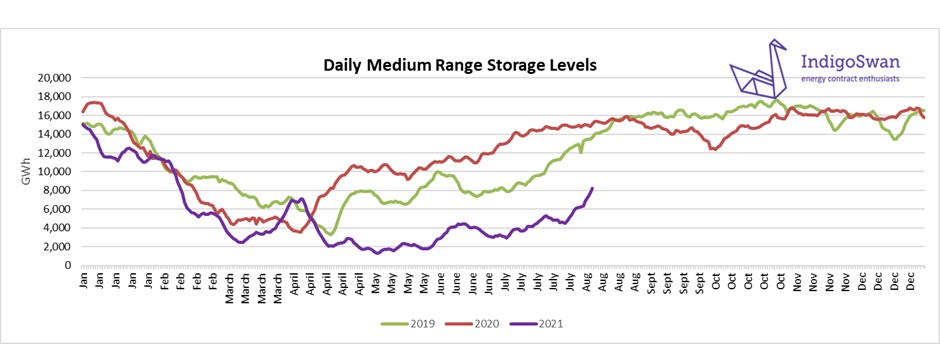

As of the 9th of August, our Medium Range Storage (MRS) levels were just 55% of those in 2020 and 60% of 2019.

In 2017 Centrica announced the closure of Rough Storage due to safety concerns and economics. This was our main facility and allowed a sense of energy security, being topped up in the warmer months and utilised in the colder.

Since that time, we have relied on MRS and additional supplies of Liquified Natural Gas (LNG) from the likes of Qatar, Australia and the USA, to top up our own domestic production and that imported from the continent. LNG deliveries have become an integral part of our Gas supply mix.

Globally we are seeing an increase in LNG demand, which means we are now competing for what are becoming increasingly valuable deliveries, whilst there have also been disruptions to supplies. Asia remains a very attractive market, where prices regularly exceed those in other regions.

The Gas Storage issue started to become apparent in April. This tends to be when we begin to divert surplus supplies into Storage, as we saw in both 2019 and 2020. However, in 2021 there were a number of factors which prevented this.

During the month of April, we saw a prolonged period of cold weather, resulting in a higher demand for both Gas and Electricity. This created a more obvious use for Gas in the form of heating, but also a 70% increase for the generation of Electricity, when compared to 2020.

With a likely target to end the use of Coal for Electricity generation in the UK by October 2024, we have become more reliant on Renewables, the largest potential contributor being Wind. In April 2020, Wind provided 18% of supplies, whilst in April 2021 this was just 13%, or when taking into consideration the higher national demand, a drop of 18% in actual Electricity generated.

Looking at April 2021 in more detail, there were days when Wind contributed between just 1% to 3% of generation and Gas a huge 55% to 60%. This demand not only meant that we were not able to store Gas but found that MRS levels were quickly being depleted.

With an awareness that Storage levels need to be considerably higher for Winter 2021, there have been attempts to increase them. However, with the global demand for LNG supplies, Gas supply outages and an increased demand to generate Electricity, progress has been slow.

The position for the remainder of 2021 remains uncertain, which explains the impact on Gas and Electricity Wholesale prices. Longer term, there is more positivity which is reflected in Winter 2022 and Winter 2023. The Nord Stream 2 pipeline from Russia into Europe is due to be completed in August 2021 and there is the capacity for further deliveries should they be utilised. This reliance on Russian Gas by Europe does cause some concern, which has hopefully been addressed in an agreement between the USA and Germany, with measures to try to avoid energy being used as a political tool.

Source data, National Grid

If you enjoyed reading this blog, take a look at some of our other blog posts here