As of the 6th of August, Gas and Electricity Year Ahead Wholesale costs were higher than those in last month’s report.

Prices initially fell in July which seemed to reflect a growing positivity. However, the lack of clear direction was an indication that it would take little to trigger a period of volatility. Towards the end of the month, a number of factors combined to add upward price pressure, which has continued into August.

Tensions have once again risen in the Middle East with the potential to interrupt Gas and Oil supplies from the region. Financial and energy markets wait to see if Iran will respond to Israel’s actions. High temperatures in parts of Asia and Europe are increasing Gas demand for air-cooling and we continue to see planned and unplanned maintenance of Gas assets which impacts both LNG and piped supplies. The contribution of Wind to generation has been modest, at 17% of supplies in July and 18% over the last week.

EU Gas Storage levels are 86% full which is comparable to last year and set to exceed the 90% target by November, likely reaching 100% before the higher winter demand begins. Norway is supplying large volumes of Gas to Europe, replacing some from Russian, but LNG shipments have reduced significantly as they are attracted to Asia, where there is a price premium.

The energy industry has changed how it recovers Electricity Distribution, Transmission and Balancing costs, under the Targeted Charging Review. This has moved some charges away from being based on the energy used and billed in the unit rate, to fixed charges incorporated within the Standing Charge or as separate items. This should give both the customer and the industry a more accurate way of calculating budgets, but the change has become noticeable within energy bills and created concern. Over the next two years, there is a quite confused picture of increases and decreases in Transmission and Distribution charges, which energy suppliers will be billing customers.

From April 2024 most customers saw a decrease in Transmission which is likely to be followed by an increase in this fixed charge from April 2025, almost completely replacing what used to be recovered through Triads. Distribution costs are a little more complicated with the average fixed annual cost increasing across networks from April 2024 but decreasing from April 2025. Another element, the Available Capacity (AC), has already seen small increases but is due for a more significant rise from April 2025. This does mean that by managing the Agreed Supply Capacity, there is an opportunity to reduce the AC cost and longer term, potentially lower the Band which determines fixed charges.

Balancing costs were lower from April 2024, with increases expected from October 2024.

Indigo Swan works closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

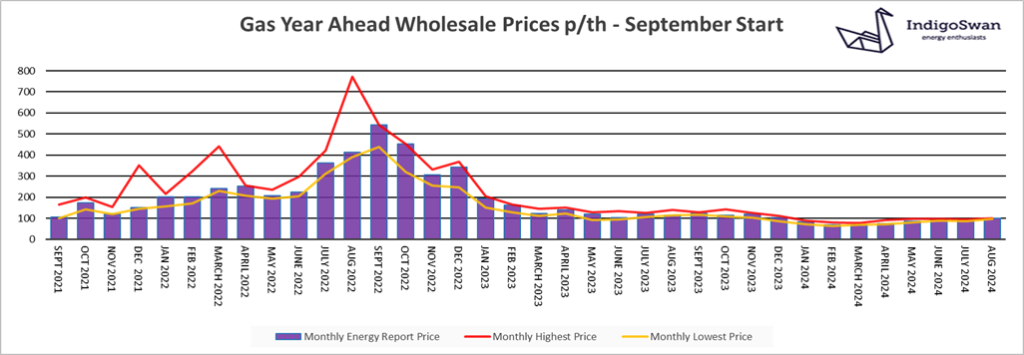

On the 6th of August, the Gas Year Ahead Wholesale cost was 99.56p/th, up from 93.24p/th in last month’s report and 14% less than 2023.

The EU Gas Storage target is 90% full by November, in order to be ready for the higher winter demand. This was surpassed last year, reaching 100%, which is likely once again as it is already 86% full. This positive position has been achieved with increased Gas flows from Norway and imports of LNG from global sources, as well as efforts to reduce demand. Europe continues to receive large volumes of Gas from Russia as sanctions would be damaging to some economies and likely create dramatic price spikes. This is unpopular with the likes of Germany and Hungary.

In recent months, LNG shipments have headed to Asia, where there is a higher demand and price. Although there is no shortage of Gas in Europe, the lack of LNG is seeing nervous market reactions when there are issues, such as interruptions to other sources or increases in demand for air-cooling.

With Wholesale prices once again on an upward trend, there is little evidence that we will see a significant downturn. It is more likely that, as we saw last summer, prices will continue to show low levels of volatility but avoid the price spikes seen in recent years. However, due to the tight global supply / demand relationship, any new event has the potential to impact on prices and so we would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

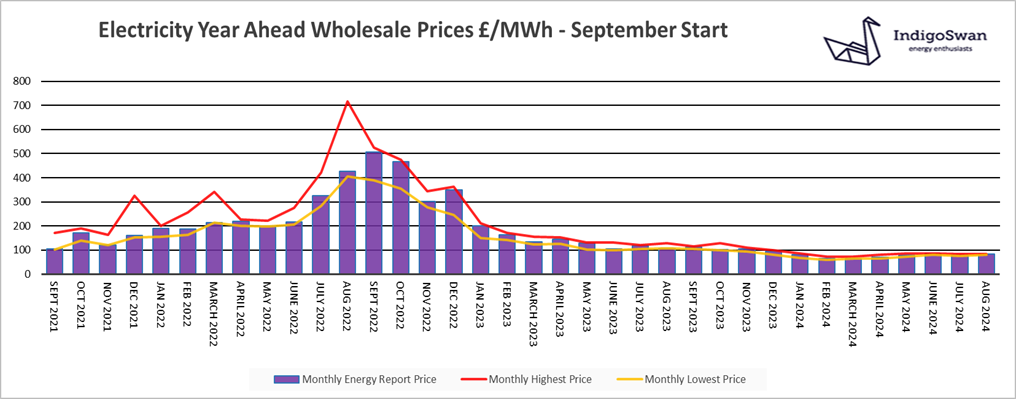

On the 6th of August, the Electricity Year Ahead Wholesale cost was £83.79/MWh, up from £82.07/MWh in last month’s report and 22% less than 2023.

The Electricity price continues to follow Gas, which is coming under pressure from a number of directions, although EU Storage remains high at 86% full. These include low levels of LNG shipments to Europe, disruptions to supplies and a higher demand for air-cooling. In July, Gas contributed 25% of generation, up from 21% in June as it compensated for lower Wind at just 17%. The last week has seen Gas at 23% and Wind at 18%.

The Interconnectors with Europe which allow Electricity to flow both ways, are becoming increasingly important, regularly providing over 20% of our supplies. Contributors include France, Norway, Denmark and Belgium, and largely sourced from Nuclear and Hydro. This avoids the need for us to build more generation and burn as much Gas or Coal.

With Wholesale prices once again on an upward trend, there is little evidence that we will see a significant downturn. It is more likely that, as we saw last summer, prices will continue to show low levels of volatility but avoid the price spikes seen in recent years. However, due to the tight global supply / demand relationship, any new event has the potential to impact on prices and so we would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

If you enjoyed reading this blog why not try one of our others: