Overview

As of the 9th June, Gas and Electricity Year Ahead Wholesale costs are slightly higher when compared to last month’s report.

Over the last month, Oil has recovered from $29 a barrel to $41. Although this appears significant, earlier in the year we saw in the region of $70. OPEC and other producers have agreed to extend their deep production cuts until at least the end of July. Recent demand increases from China and other nations easing lockdown measures, may address significant global stockpiles.

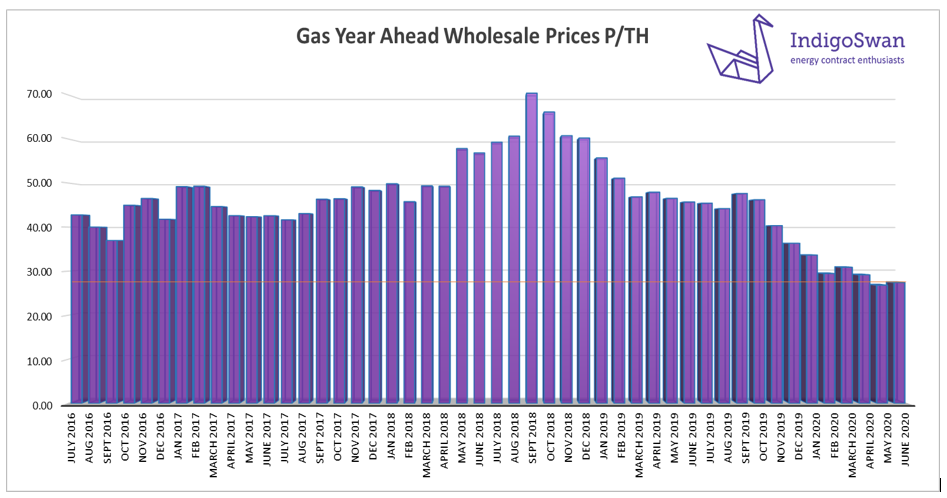

Gas Wholesale costs are very competitive, as illustrated by our graph. May saw another month of high LNG deliveries, which have continued into June, due to a low global demand. Use for generation was down to 29% from 32% in April.

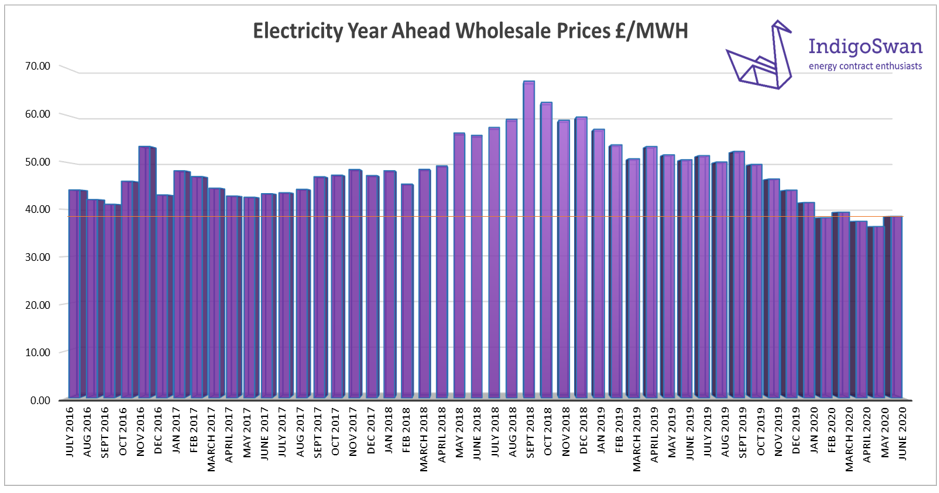

Electricity Wholesale prices are at 2016 levels. Wind’s contribution was down to 17% from February’s record breaking 29%. Some of this shortfall was made up by additional Solar at 10%. Coal is a more expensive form of generation and has not been used for two months. Coal power stations continue to close early, prior to a full shut down by 2024, to help meet carbon reduction targets.

The Met Office forecast for the next month suggests mixed unsettled conditions. Some regions will see cool wet and windy weather, whilst mainly in the south, there is the potential for warmer periods. The Renewables contribution is likely to be modest, requiring some more use of Gas generation.

What does this mean for me…?

Wholesale prices show very good value, but it should be remembered that the Wholesale element makes up in the region of just 40% of the total cost of an Electricity bill. Gas is roughly 55%.

The influence of higher third-party costs is increasingly noticeable in Electricity contracts. These include, Transportation, Distribution and government policy levies.

Over the next few years, the way some of these charges are calculated will change, under the Targeted Charging Review, although the details are not yet available. Initially the first change to Transportation costs was due April 2021, but with delays issuing price guidelines to energy suppliers, this has been postponed until April 2022. The planned change to Distribution charges is still set for April 2022. This does mean that the expected opening of some fixed priced contracts should not take place until 2022.

To benefit from the low Wholesale prices, we advise requesting supplier offers for all 2020 and early 2021 start contracts. Be aware that suppliers are tightening their credit requirements and reducing their risk appetite, but good forward contract options can still be negotiated.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas Market

On the 9th June, the Gas Year Ahead Wholesale cost was 27.41 (p/th), from 26.82 (p/th) in last month’s report and 40% lower than 2019.

There were sixteen LNG deliveries in May, with the impact of the coronavirus reducing global demand and prices. Although some regions are easing lockdown measures, as with the UK, European Storage levels are high for the time of year, reducing the expectation for a large increase in demand, beyond available supply. This provides a degree of confidence.

Gas use was low again in May, with many businesses closed and a reduction in the use for generation, due to a high Renewables contribution. June will likely see some recovery, but with no current supply concerns, this should add little pressure to prices.

Oil does have some contractual links with Gas. This could add an upward pressure should production cuts and a global recovery, move the Oil price higher.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

Electricity Market

On the 9th June, the Electricity Year Ahead Wholesale cost was 38.53 (£/MWh), from 36.37 (£/MWh) in last month’s report and 23% lower than 2019.

The continued reduction in the national Electricity demand since the coronavirus required the closure of many businesses, has meant that at times we have surplus supplies. This has resulted in no Coal generation for two months and less need for Gas. Although May saw a slight reduction in Wind at 17%, Solar contributed a record 10% to generation. So far in June they have a combined 24%, with Gas increasing from 29% to 35%.

With Gas being the main source of generation, the Electricity Wholesale cost follows, despite the increased influence of Renewables. The decision by Oil producers to support prices with extended deeper cuts, may result in higher Gas and Electricity prices, as global activity increases.

Third Party Charges continue to increase regardless of how the Wholesale element changes. These charges typically pay for the mechanisms, securing generation at peak periods.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.