Headlines:

- Gas and Electricity Wholesale prices are higher than last month

- Prices continue to react to small changes in supply and demand

- EU Gas Storage levels are a high 59% full

Energy Overview

As of the 1st of April, Gas and Electricity Year Ahead Wholesale costs were higher than those in last month’s report.

The three-year low prices we saw in February, have since increased, struggling to find direction with daily swings of up to 5%. The nervousness within the industry is largely due to the pressure on global Gas supplies, with Europe looking to replace those that previously came from Russia. LNG shipments have increased, notably from the US, making them the biggest exporter.

Thoughts are already turning to the level of Gas Storage held by the EU, which is required to help meet the additional winter heating demand. Currently at 59% full, this is a very positive position and higher than the 56% last year and 25-30% the previous two years, when there was a real concern that customers could potentially see restrictions on Gas use.

Despite there being more Renewable assets, there remains a need for Gas to provide a reliable source of generation and have the flexibility to react to additional peak demand or replace lower Wind and Solar. In March, Gas use for generation fell to just 26% of Electricity supplies, down from 28% in February. This was due to high Wind, Solar and Interconnector contributions.

What does this mean for me?

The Energy Bills Discount Scheme (EBDS) ended on 31st March 2024. It was designed to give all non-domestic customers, including the voluntary sector (such as charities) and the public sector (such as schools and hospitals) access to a phased in maximum discount when the customer’s wholesale cost exceeded the defined thresholds. Suppliers automatically applied discounts. The price of Gas and Electricity has fallen considerably since the scheme’s introduction. Those companies classed as Energy and Trade Intensive Industries (ETII) and Heat Networks, had to apply to receive a more attractive discount.

Over the last few years, the energy industry has changed the way it recovers Distribution, Transmission and Balancing costs, under the Targeted Charging Review. This has resulted in moving some charges away from being based on the energy used and billed in the unit rate, to fixed charges incorporated within the Standing Charge. In theory this should give both the customer and the industry a more accurate way of managing finances, but the increases have become more noticeable within energy bills and give less scope to reduce costs through energy management. From April 2024 it is expected most customers will see a reduction in Electricity Distribution costs over the next year, but higher Transmission charges. Balancing costs will be lower for six months, before increases are expected from October 2024.

Indigo Swan are working closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

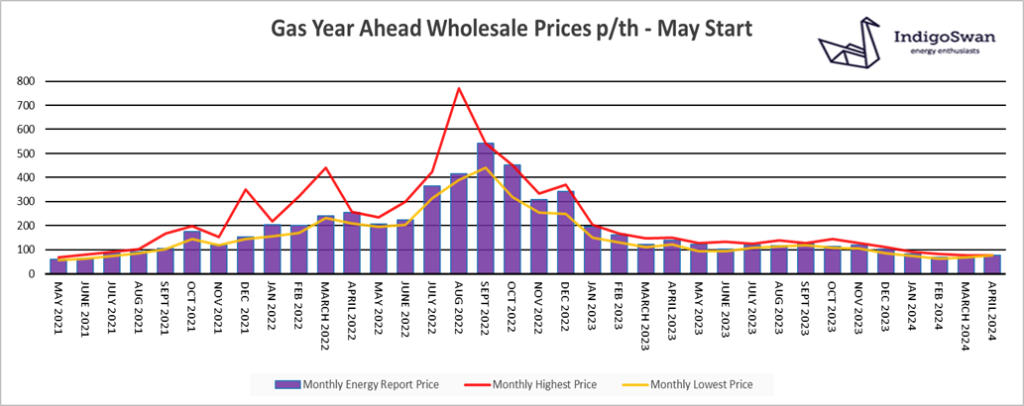

Gas market overview

On the 1st of April, the Gas Year Ahead Wholesale cost was 76.54p/th, up from 69.43p/th in last month’s report and 45% less than 2023.

The positive level of EU Gas Storage means that prices are considerably lower than seen through the volatility of the last three years, although we did see better value in February and March 2024.

The EU continues to receive large amounts of LNG. Although tensions in the Middle East threaten shipping passing through the Suez Canal via the Red Sea, so far there has been little actual disruption. However, there is the potential that long term, the US government may restrict any new LNG export projects, to consider the impact on domestic energy costs and carbon emissions. Qatar has outlined plans to increase production to capitalise on a growing global demand.

The high level of EU Gas Storage at 59% full is providing a degree of optimism that the target to replenish stocks to 90% full by November can be met, in readiness for winter 2024/25. With the delicate balance between supply and demand, any number of events could still impact on prices, such as further developments in the Middle East, resulting in the cancellation of Gas shipments. We have also seen unplanned LNG restrictions from the US. Europe has been extremely fortunate that since Gas shortages began in 2021, there has not been a period of prolonged extremely cold temperatures, which have the potential to create price spikes.

We would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

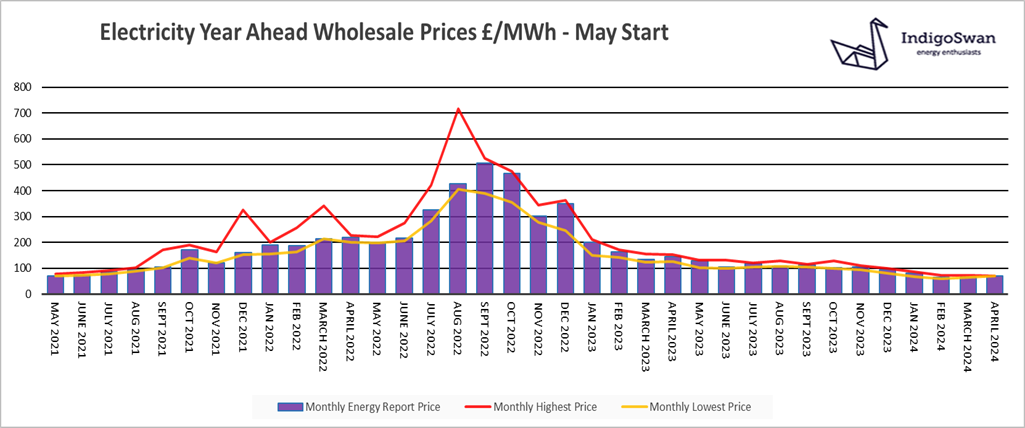

Electricity market overview

On the 1st of April, the Electricity Year Ahead Wholesale cost was £70.07/MWh, up from £65.06/MWh in last month’s report and 52% less than 2023.

A very high 20% contribution of supplies in March from the Interconnectors with Europe, meant a reduced need for Gas, which still provided 26%. Gas dictates Electricity’s price direction as it is a reliable source of generation and replaces lower Renewables. A number of global issues, such as the tensions in the Middle East, disruption to LNG supplies or imports of Gas from Norway, as well as a severe cold spell, have the potential to impact on Electricity prices. Wind provided a lower 28% from 30% the previous month, although far higher than the 25% last year. At just over 1% of supplies, we continue to use Coal to help balance the network, before it finally stops later this year. The National Grid will be using more creative tools to cope with peak demand.

The government has outlined the need for new Gas and Nuclear generation as well as further Interconnectors, all of which will be essential to ensure we are able to make the transition to Electricity, from using Gas for generation and heating. Significant investment will also be needed to move power across the UK, linking Wind farms and Solar to areas of high demand. Ideally, we should be able to store surplus Renewables, but at this time the projects are small scale, providing another option to help at times of high demand.

We would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

If you enjoyed reading this blog why not try one of our others: