Headlines:

- Gas and Electricity Wholesale prices are similar to last month

- A more positive outlook this winter compared to last

- EU Gas Storage ae a very high 99% full

Energy Overview

As of the 7th of November, Gas and Electricity Year Ahead Wholesale costs were similar to those in last month’s report.

Gas Storage levels in the EU are almost 100% full against a target of 90%. As a result of this and a generally more optimistic outlook this winter, energy prices are considerably lower than November 2022. We did see some price volatility in October with the conflict between Israel and Hamas generating concern that there could be supply restrictions from the region, if other countries were drawn in. There was also damage to a Gas pipeline between Finland and Estonia with the suspicion that it could be a similar act of sabotage to that seen in 2022 to Nord Stream. The investigation has found that the damage was done by a ship’s anchor, allowing for the possibility this was an accident and reducing the likelihood that other Interconnectors would be targeted.

Gas is the main source of generation, despite the growing diversity of Electricity supplies, such as from renewables and connections to the continent. However, due to the lack of reliability of Wind and Solar, and not currently being able to store Electricity on any great scale, Gas generation continues to dictate prices.

The Met Office forecast for November suggests temperatures are likely to be in the region of seasonal norm.

What does this mean for me?

The Energy Bills Discount Scheme (EBDS) replaced the Energy Bill Relief Scheme (EBRS) on the 1st of April 2023. It is designed to give all non-domestic customers, including the voluntary sector (such as charities) and the public sector (such as schools and hospitals) access to a phased in maximum discount when the customer’s wholesale cost exceeds the defined thresholds. This scheme lasts for 12 months until 31st of March 2024 and applies to contracts that were put in place on or after 1st of December 2021 and non-contracted arrangements. As with the EBRS, energy suppliers will automatically apply these standard discounts. The levels of assistance are less generous, but the price of Gas and Electricity is considerably lower than 2022. Those companies that are classed as Energy and Trade Intensive Industries (ETII) and Heat Networks, had to apply in July 2023 to receive a more attractive discount.

Customers may have started to see higher Standing Charges on their Electricity invoices from 1st of April 2023. There have been changes to the way some industry charges are calculated, under the Targeted Charging Review. This move is part of an attempt to recover more Electricity costs, such as Transmission and Balancing, through fixed fees. In theory this should give both the customer and the industry a more accurate way of managing finances.

Indigo Swan are working closely with energy suppliers to help all our customers understand and manage these changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

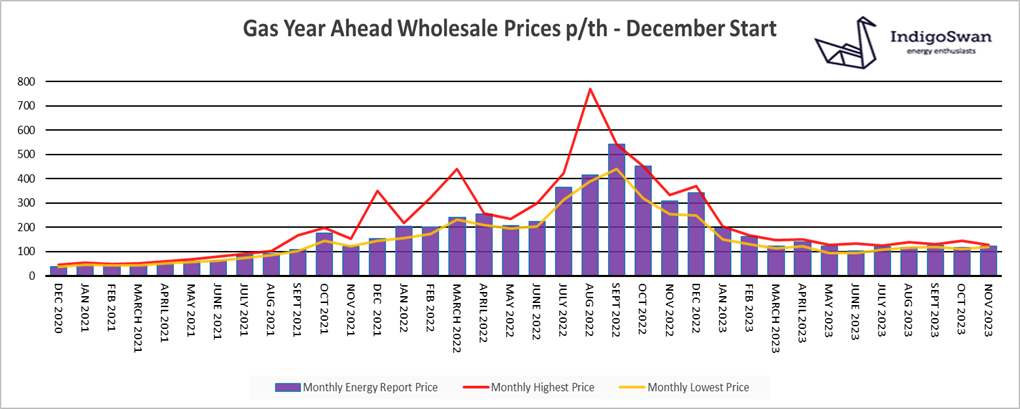

Gas market overview

On the 7th of November, the Gas Year Ahead Wholesale cost was 120.41p/th, up from 114.94p/th in last month’s report and 61% less than 2022.

Despite the price volatility seen in October in response to the attack by Hamas on Israel and the subsequent military action in Gaza, markets have settled, due to it being contained. There remains the possibility of the conflict spreading to other nations, with the resulting impact on supplies through possible infrastructure damage, blockades and sanctions. The security of Gas pipelines was once again a concern as it was thought an unfriendly nation may have targeted the Finland to Estonia Interconnector, highlighting the vulnerability of others.

EU Gas Storage levels continue to increase, now at 99% full against a November target of 90%, from when it is assumed that a higher Gas demand for heating and Electricity generation may mean Gas withdrawals. LNG deliveries continue to be made to Europe, which are an important replacement for the reduced flows from Russia.

It is currently being assumed that we will have seasonal normal temperatures this coming winter and that there will be no interruptions to imports into Europe or unplanned closures of assets. Any domestic or global events which may reduce Gas supplies or increase demand, will have an exaggerated effect. The Groningen Gas field has now closed due to safety concerns but could be utilised for one more year in the event of a Gas supply emergency.

We would advise discussing your options for contracts ending in 2023 or early 2024 with Indigo Swan.

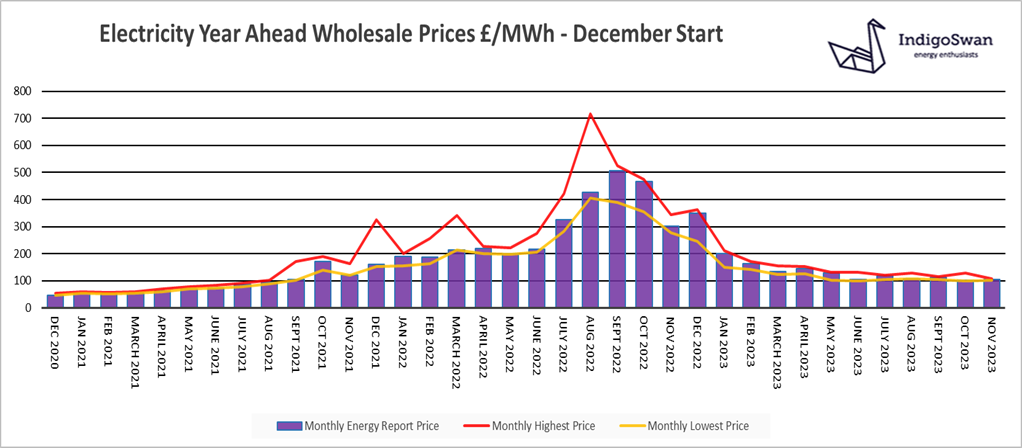

Electricity market overview

On the 7th of November, the Electricity Year Ahead Wholesale cost was £104.56/MWh, up from £103.56/MWh in last month’s report and 65% less than 2022.

With 29% of Electricity generation coming from Gas in October and in comparison to other sources, being very reliable and flexible, Electricity prices will continue to follow the daily ups and downs of Gas. Wind also accounted for 29%, although its erratic nature did mean one day was as low as 7% and in the last week reached 38%.

The “cautious optimism” expressed by the National Grid ESO remains for the winter. We have more generation available, battery storage and tools such as the Demand Side Response and the Demand Flexibility Service. It is likely that as long as temperatures remain within the boundary of normal, that consumers will use less Gas and Electricity this year, as they did last, in order to reduce the impact of high energy costs. We are seeing an increased connectivity with mainland Europe, with Hydro Electricity coming from Norway and Nuclear from France. Coal is still being used by the ESO to balance the grid when margins are tight.

Although the large number of non-energy charges predominantly built into Electricity prices add to costs, they do and help protect us from power shortages and more erratic wholesale costs.

Let us know if you would like us to research your options for contracts ending in 2023 or early 2024.

If you enjoyed reading this blog why not try one of our others: